Auto insurance is one of those expenses that many people accept as fixed and unavoidable. Month after month, premiums are paid without much thought, even though the cost can quietly increase over time. In reality, auto insurance rates are not set in stone. There are many practical, legal, and effective ways to lower your auto insurance without sacrificing the protection you need.

Understanding how insurance companies calculate premiums is the first step toward saving money. Factors such as driving history, vehicle type, coverage choices, location, and even personal habits all play a role. By making informed decisions and small adjustments, you can significantly reduce your auto insurance costs over the long term.

Below are 10 real and proven ways to lower your auto insurance, explained in a natural, human-written style that focuses on clarity, usefulness, and real-life application.

1. Shop Around and Compare Insurance Providers

One of the biggest mistakes drivers make is staying with the same insurance company for years without comparing options. Loyalty does not always lead to lower rates. Insurance companies use different formulas to calculate risk, which means the same driver can receive very different quotes from different providers.

Shopping around allows you to see the full picture of the market. Comparing at least three to five quotes can reveal significant savings. Some insurers specialize in certain driver profiles, such as safe drivers, low-mileage drivers, or families with multiple vehicles.

When comparing policies, look beyond the price. Make sure coverage limits, deductibles, and benefits are similar so you are making a fair comparison. A slightly higher premium may still offer better value if the coverage is stronger.

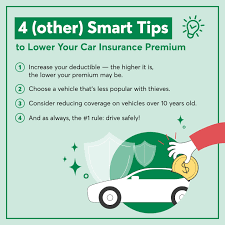

2. Increase Your Deductible

Your deductible is the amount you pay out of pocket before your insurance coverage applies. A lower deductible means the insurance company pays more when a claim is filed, which usually results in higher premiums.

By increasing your deductible, you can lower your monthly or annual insurance costs. For example, raising your deductible from $500 to $1,000 can lead to noticeable savings. However, this strategy only works if you have enough savings to cover the higher deductible in case of an accident.

Choosing the right deductible is about balance. You want lower premiums without putting yourself in a risky financial position if a claim becomes necessary.

3. Maintain a Clean Driving Record

Your driving history is one of the most important factors in determining your auto insurance rate. Accidents, speeding tickets, and other violations signal higher risk to insurers, which leads to increased premiums.

Driving safely and responsibly over time can significantly reduce your insurance costs. Many insurance companies offer safe driver discounts for drivers who maintain a clean record for several years.

Avoiding distractions, obeying speed limits, and practicing defensive driving not only protect your safety but also protect your wallet. In the long run, careful driving is one of the most effective ways to keep insurance costs low.

4. Take Advantage of Discounts

Insurance companies offer a wide range of discounts, but many drivers are unaware of them or forget to ask. Common discounts include good driver discounts, good student discounts, multi-vehicle discounts, and low-mileage discounts.

Other discounts may be available for completing defensive driving courses, installing safety features, or maintaining continuous coverage. Some insurers also offer discounts for paperless billing or automatic payments.

It is important to review available discounts regularly. Life changes such as graduating, retiring, or changing jobs may qualify you for new savings opportunities.

5. Bundle Your Insurance Policies

Bundling multiple insurance policies with the same provider is a popular and effective way to reduce costs. Many insurers offer discounts when you combine auto insurance with home, renters, or life insurance.

Bundling simplifies your financial management by reducing the number of bills and policies you need to track. It also strengthens your relationship with the insurer, which can sometimes lead to better customer service and additional benefits.

Before bundling, compare the bundled price with separate policies from different providers to ensure the discount truly offers savings.

6. Choose the Right Vehicle

The type of car you drive has a major impact on your auto insurance rate. Vehicles with high repair costs, powerful engines, or high theft rates tend to be more expensive to insure.

If you are planning to buy a new or used car, consider insurance costs as part of your decision. Cars with strong safety ratings, advanced safety features, and lower replacement costs usually qualify for lower premiums.

Luxury cars and sports cars may be appealing, but they often come with significantly higher insurance costs. Choosing a practical vehicle can lead to long-term savings.

7. Review and Adjust Your Coverage Regularly

Many drivers carry coverage they no longer need. As your vehicle ages and its value decreases, certain types of coverage may become less cost-effective.

For example, if your car is older and fully paid off, comprehensive and collision coverage may cost more than the car’s actual value over time. Reviewing your policy annually helps ensure you are not overpaying.

At the same time, never reduce coverage below legal requirements or your personal risk tolerance. The goal is to optimize coverage, not eliminate protection.

8. Improve Your Credit Score

In many regions, insurance companies use credit-based insurance scores to help determine premiums. A higher credit score often indicates financial responsibility, which insurers associate with lower risk.

Improving your credit score by paying bills on time, reducing debt, and monitoring your credit report can lead to lower insurance costs over time.

Although credit is not directly related to driving ability, its influence on insurance pricing is significant. Maintaining good credit supports savings across multiple areas of your financial life.

9. Limit Mileage and Usage

The more you drive, the higher the risk of accidents. Insurance companies consider annual mileage when calculating premiums. Drivers with lower mileage are often rewarded with lower rates.

If you work from home, carpool, or use public transportation, inform your insurer. You may qualify for low-mileage discounts or usage-based insurance programs.

Some insurers offer telematics programs that track driving behavior and mileage through a mobile app or device. Safe driving habits can lead to personalized discounts.

10. Avoid Small Claims and Build Insurance History

Filing frequent small claims can increase your insurance premiums over time. While insurance exists to protect you in serious situations, using it for minor repairs may not always be beneficial.

Paying for small damages out of pocket can help preserve a clean claims history. Many insurers reward claim-free drivers with lower premiums and loyalty benefits.

Building a long-term insurance history with responsible usage demonstrates reliability and reduces perceived risk.

Final Thoughts

Lowering your auto insurance is not about cutting corners or accepting unnecessary risk. It is about making informed choices, understanding how premiums are calculated, and actively managing your policy.

By shopping around, maintaining safe driving habits, choosing the right vehicle, and regularly reviewing coverage, you can achieve meaningful savings without compromising protection. Auto insurance should work for you, not against you.

With the right strategy and consistent attention, lowering your auto insurance is not only possible but achievable for almost every driver.

Summary:

Nowadays, auto insurance is really expensive. A typical insurance policy can cost a few hundred dollars to a few thousand dollars a year.

Keywords:

Car Inurance, Car, Inusrance, Finance, Business

Article Body:

And the insurance rates you pay are hugely dependent on the insurance company or agent, your age, your car type, your driving record, and even the area you reside in!

You should never go without auto insurance though, despite the costs. Almost all the states require you to protect yourself with a minimum amount of liability coverage. Naturally, the bare minimum is not adequate enough for the average car owner. And as you add in additional coverage for your car, you realize that you will be paying a fairly large sum annually.

So, understanding auto insurance can actually help you to decide on a suitable insurance policy that won’t vacuum clean your wallet! Here, we have gathered 10 of the best tips for lowering your auto insurance, by as much as 40%!

Always compare insurance policies. There are states which regulate auto insurance rates, but the insurance premiums can vary by hundreds of dollars for the exact same coverage. It is definitely worthwhile to shop around. The first thing you can do is to check with your state insurance department. They often provide information about the coverage you need, as well as sample rates from the biggest companies. You can also ask your friends or look up the yellow pages. Checking consumer guides and asking insurance agents can pay off as well. You can easily find out the price range for your insurance policy, as well as discover the lowest prices in town.

However, you should not be shopping based on price along. The insurance company should provide good service at the best price. Excellent personal service is available as well, and they provide added conveniences, although they cost a fair bit more. Ask the company how you can lower your costs, and also check their financial ratings. The rule of thumb is always to get three price quotes from three different companies, and pick the one with the best value.

It can also be a good idea to increase your deductibles. When you file a claim, the deductible is the amount you pay before the insurance company pays for the rest of the damage. A higher deductible on collision and comprehensive coverage can lead to a much lower premium. For example, increasing your deductible from $200 to $400 can reduce your premiums by up to 25%. However, you must ensure that you have the financial resources to handle the largest deductible when the time comes.

Remove certain types of coverage from your policy. Almost all the states require liability coverage for your car, but the rest of the coverage is probably dispensable. However, you do not want to be underinsured if you’re in an accident, so it isn’t advisable to remove all of your additional coverage. Optional coverage includes medical payments, uninsured motorist, collision, and comprehensive coverage.

Drop collision and comprehensive coverage for older cars. If you drive an older car that’s worth less than $2,000, it’s probably more cost-effective to drop collision and comprehensive coverage since you’ll probably pay more for the coverage than you’ll collect for a claim. You can find out the worth of your car by asking auto dealers and banks.

Make sure your credit report looks good. Car insurance companies often look at your credit history as there is a correlation between the risk to the company and your credit history. If you pay your bills on time and maintain a good credit history, you can enjoy lower insurance rates.

Drive less. Insurance companies often offer low-mileage discounts to motorists who drive less than a predetermined number of miles each year. You can use public transportation more often, car-pool with friends, and take the train or a plane instead of driving to another state. And you’ll save on more than your coverage as you’ll need to spend less on gasoline (of which prices are incredibly high).

Maintain a clean driving record. The company will give you a price break and you can save on your insurance policy after a specified period of a clean driving record. This means that you have no accidents, no serious driving violations etc, during this period of time. The simplest and surefire way to qualify for this discount is to drive carefully and defensively all the time.

Choose a low-profile car. Insurance rates vary among difference models of vehicles. Generally, sports cars and high-performance cars tend to cost more to insure, mainly because they represent more risk of theft and the drivers are often the people who drive more recklessly. Newer cars will cost more to repair or replace than older ones, so naturally they can more to insure. Low-risk vehicles include station wagons and sedans.

Ask about safety and security discounts. The insurance companies sometimes offer discounts on your insurance if your car is equipped with the following: anti-lock brakes, air bags, automatic seat belts, car alarms, tracking systems. These reduce the injury risk to you, as well as the chances of your car being vandalized or stolen.

Finally, ask about other discounts. You may receive a discount if you buy more than one type of insurance from the same company or if you insure multiple cars under the same policy or company. You may also receive discounts for taking a defensive driving course, staying with the same company for a few years, being a driver over 50, good-student discounts, and being an AAA member. If you already have adequate health insurance, you can also eliminate paying for duplicate medical coverage, thus lowering your personal injury protection costs by a substantial amount.

Tinggalkan Balasan